Introduction

According to Cantaloupe's 2025 Micropayment Trends Report, 71% of all vending machine sales in 2024 were cashless—a 17% year-over-year increase. For vending operators, that shift has fundamentally changed the cost structure of doing business. Credit card processing fees are no longer a minor line item; they're a make-or-break operational expense.

The challenge is that processing fees in vending aren't a flat, predictable number. They vary based on fee structure, processor, transaction size, card type, and location—and misunderstanding them is one of the fastest ways to erode already thin margins.

When your average transaction is under $2.50 and your net margin hovers between 20-30%, a processing fee that consumes 8-10% of revenue can wipe out a third of your profit on every sale.

This guide breaks down exactly how credit card processing fees work in vending, why they hit small-ticket operators harder than any other business, and the specific strategies you can use to protect your margins without sacrificing the cashless convenience customers now expect.

Key Takeaways

- Credit card processing fees for vending machines run 1.5%–3.5%, but flat per-transaction fees (e.g., $0.10) push the true cost far higher on small-dollar sales

- Three fee layers stack together: interchange (set by card networks), assessment fees (card brand charges), and processor markup (the only negotiable piece)

- Visa and Mastercard small ticket interchange programs can substantially lower rates — if your operation qualifies

- To reduce fees: qualify for small ticket rates, negotiate processor markup, revisit pricing strategy, and choose payment-ready machines upfront

Why Credit Card Fees Hit Vending Operators Harder Than Other Businesses

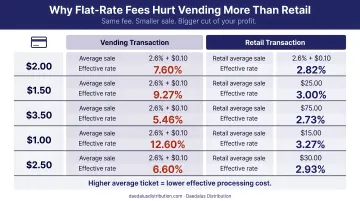

Vending faces a brutal math problem that few other industries encounter: exceptionally low average transaction values combined with fixed-cost processing structures. The average cashless vending transaction in 2024 was $2.24, and the total average (including cash) was $2.11.

Here's why that matters:

Credit card processing fees include both a percentage component and a flat per-transaction fee. That flat fee—typically $0.10 or more—becomes an outsized percentage of the sale on low-dollar transactions.

The math on a typical $1.75 candy bar:

Using a common processing structure of 2.6% + $0.10:

- Percentage fee: $0.05 (2.6% of $1.75)

- Flat fee: $0.10

- Total fee: $0.15

- Effective rate: 8.6% of revenue

Compare that to the same fee structure on a $25 retail purchase:

- Percentage fee: $0.65 (2.6% of $25)

- Flat fee: $0.10

- Total fee: $0.75

- Effective rate: 3.0% of revenue

The flat fee becomes negligible at higher ticket sizes but dominates at vending-scale transactions.

How this interacts with vending margins:

Vending operators typically run on net profit margins of 20-30%, with gross margins often falling between 40-60% depending on product mix and location. When an 8-10% processing fee hits revenue, it consumes roughly one-third of gross margin on that transaction before you've paid for labor, route costs, or machine maintenance.

Vending isn't alone, but it's especially vulnerable:

Other unattended payment environments face similar challenges, but vending's consistently low ticket size amplifies the impact:

- EV charging: Average $30 per session

- Parking meters: Typically $5+ per transaction

- Vending: $2.24 average cashless transaction

At $2.24 average, vending sits well below any other unattended payment category — which is why the same processing structure costs vending operators nearly three times as much of their revenue as it costs a typical retailer.

Additional vending-specific costs:

Beyond the per-transaction rate, vending operators also pay:

- Cellular data fees for card reader connectivity (typically $3.99-$9.99/month per machine)

- EMV compliance requirements for unattended terminals

- PCI DSS compliance fees (sometimes charged separately by processors)

- Hardware costs for cashless terminals (upfront or leased)

For a 10-machine route, cellular data fees alone can add $40-$100/month before a single transaction is processed — a fixed cost that hits small operators and large fleets alike.

What Are Typical Vending Machine Credit Card Processing Fees?

Processing a card payment in vending isn't a single charge. Your total cost is built from several layers, each billed by a different party — and understanding each one is how you avoid overpaying.

Interchange Fees

Interchange fees go to the card-issuing bank and are set by the card networks — Visa, Mastercard, and others. These are non-negotiable.

Standard interchange rates for credit card transactions range from 2.0% to 2.24% plus a per-transaction fee. Debit cards and prepaid cards generally carry lower rates.

Small ticket interchange programs:

Visa and Mastercard both offer reduced interchange rates for businesses where a qualifying percentage of transactions fall below specific thresholds. For vending operators with small average ticket sizes, these programs can meaningfully lower the base interchange cost.

Key small ticket interchange rates (2025-2026):

| Network | Program | Rate | Qualification |

|---|---|---|---|

| Visa | CPS/Small Ticket, Debit | 1.55% + $0.04 | PIN-authenticated Visa Debit |

| Mastercard | Small Ticket Base | 1.55% + $0.04 | Transactions $5 and below |

| Mastercard | Convenience Purchases Base | 1.65% + $0.04 | 60% of transactions ≤$20 |

Source: Visa USA Interchange Rates and Mastercard 2025-2026 Interchange Programs

Qualifying for these programs requires the correct Merchant Category Code (MCC) — for vending operators, that's MCC 5499 (Miscellaneous Food Stores: Convenience Stores, Markets, Specialty Stores, and Vending Machines).

Assessment Fees

Assessment fees are charged by the card network (Visa, Mastercard, etc.) for use of their payment rails. Unlike interchange, assessment fees are a small percentage of monthly sales volume, not charged per-transaction.

Current published assessment rates:

- Visa: 0.1017% of transaction volume

- Mastercard: 0.1017% (with an additional Acquirer Volume Assessment Fee of 0.090% effective July 2025)

These fees are also non-negotiable but represent a relatively small portion of total processing costs.

Payment Processor / Gateway Fees

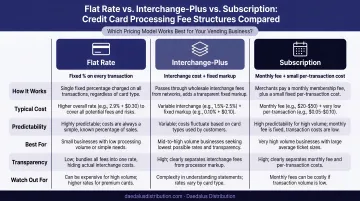

Unlike interchange and assessment fees, processor markup is negotiable. This is what your payment gateway or merchant acquirer charges for facilitating the transaction, providing hardware, and handling settlement — and it's where most operators have room to shop around.

Three common pricing structures:

Flat-rate pricing (e.g., 2.6% + $0.10 per transaction)

- Predictable and simple

- Potentially expensive for small tickets

- Common with all-in-one providers

Interchange-plus pricing (actual interchange + a fixed markup)

- More transparent

- Often better for volume operators

- Requires understanding of interchange categories

Subscription/flat-fee (monthly fee + small per-transaction cost)

- Suited for high-volume operators

- Lowers per-transaction cost

- Requires minimum transaction volume to be cost-effective

Vending-focused processor rates (2025):

| Provider | Hardware Cost | Monthly Service | Transaction Fee |

|---|---|---|---|

| Cantaloupe (ePort Engage) | $329.95 | $9.95/month | 5.95% flat |

| Nayax (VPOS Touch) | $399 | $7.95-$9.99/month | 5.95% flat OR 2.5% + $0.10 |

| PayRange (BluKey) | $35 activation | $3.99-$4.50/week | 4.25% + $0.55 compliance fee |

Flat rates like 5.95% run two to three times higher than base interchange rates. That gap is pure processor margin — worth negotiating if your volume justifies it.

Additional Vending-Specific Costs

Beyond the processing rate, operators face recurring costs that are often overlooked:

- Cellular data plans for card reader connectivity ($3.99-$9.99/month per machine)

- Hardware costs for cashless terminals (one-time purchase or lease)

- PCI DSS compliance fees (if charged separately by processor)

- Batch/settlement fees (some processors charge per settlement)

Some processors bundle these costs into monthly service fees, while others itemize them separately. Always calculate the total monthly cost per machine, not just the transaction rate.

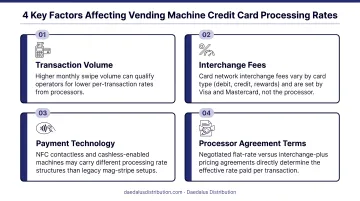

Factors That Affect Your Vending Machine Processing Rate

Your effective processing rate depends on four key variables:

- Card type: Debit and non-rewards cards carry lower interchange rates. Premium rewards and corporate cards can hit 3.0% or more — and you can't control which card a customer swipes. Card mix varies significantly by location.

- Average ticket size: The flat per-transaction fee dominates at low price points. A $0.10 flat fee is 5.7% of a $1.75 sale but drops to just 2% on a $5.00 sale.

- Transaction volume: Higher volume across your fleet gives you leverage to negotiate processor markup. Operators clearing $10,000+ monthly can often secure better rates than single-machine operators.

- Processor and pricing structure: Not every processor offers small ticket interchange programs, and not every pricing structure suits low-dollar transactions. The processor you choose matters as much as the rate they quote.

The "High Roller Effect"

If your vending machines are located in venues where customers tend to use premium rewards cards—airports, stadiums, upscale office buildings—the interchange costs on those machines will be higher than machines in budget-conscious locations.

When all machines share the same payment account, those high-cost locations pull up your effective rate across the entire fleet. Separating high-interchange locations onto different payment accounts lets you optimize rates for machines that qualify for small ticket programs.

Merchant Category Code (MCC) Matters

Vending machines typically use MCC 5499 (Miscellaneous Food Stores: Convenience Stores, Markets, Specialty Stores, and Vending Machines). Ensuring the correct MCC is assigned is essential for qualifying for small ticket interchange rates. If your processor assigns the wrong MCC, you may be paying standard interchange rates when you should be paying reduced small ticket rates.

How to Lower Credit Card Processing Fees on Your Vending Machines

Strategy 1: Qualify for Small Ticket Interchange Rates

Confirm with your payment provider that you are actually receiving small ticket interchange rates, not standard rates. Not all processors offer access to these programs, and some may not automatically enroll you even if you qualify.

Qualification requirements:

- Correct MCC assignment (typically MCC 5499)

- Meet network-specific thresholds (e.g., 60% of transactions ≤$20 for Mastercard Convenience Purchases)

- Processor must manage compliance and report to Visa/Mastercard quarterly

Ask your processor directly: "Are my vending machines enrolled in Visa and Mastercard small ticket interchange programs, and if not, why not?"

Strategy 2: Negotiate the Processor Markup

While interchange and assessment fees are fixed, the processor's markup is 100% negotiable. Operators with larger machine fleets or higher transaction volume have the most leverage.

How to negotiate effectively:

- Collect competing quotes from 3+ vending-focused processors

- Share your current effective rate and monthly volume

- Ask specifically about access to small ticket interchange programs

- Use competing offers as negotiating leverage with your current provider

Even a 0.5% reduction in processor markup can translate to hundreds or thousands of dollars annually depending on your volume.

Strategy 3: Adjust Pricing and Surcharge Strategy

Differential pricing (cashless vs. cash):

Set a higher price for cashless payments than for cash payments to offset processing costs. This is legal in most states and does not require the same disclosure as a surcharge.

Surcharges:

If differential pricing doesn't fit your operation, adding a convenience fee on cashless transactions is another option — though surcharge rules vary by state:

States where surcharges are prohibited:

- Connecticut

- Massachusetts

- Puerto Rico

In states where surcharges are legal, you must:

- Disclose the surcharge clearly at point of entry and point of sale

- Limit surcharges to the lesser of your merchant discount rate or 3%

- Display surcharge notices in minimum 16-point Arial font on unattended terminals (per Visa surcharging rules)

Credit card minimum purchase:

Under the Dodd-Frank Act, businesses can legally set credit card minimums up to $10. This allows you to offset fixed-cent interchange costs by ensuring a baseline transaction size.

Strategy 4: Choose the Right Machines and Payment Infrastructure from the Start

Operators who invest in digital vending machines with built-in cashless payment systems — such as Vendekin machines distributed by Daedalus Distribution — sidestep the aftermarket card readers, disconnected data plans, and mismatched processors that inflate costs for older fleets.

Why integrated payment infrastructure matters:

- Eliminates third-party card reader purchases with built-in payment hardware

- Configured to qualify for small ticket interchange from day one, not retrofitted later

- Provides transaction-level data visibility so you can track and optimize effective rates by location

- Bundles connectivity and support to reduce the hidden monthly fees that compound across a fleet

For operators building or expanding a fleet, this approach removes cost friction before it starts.

Strategy 5: Analyze Transaction Data by Location

Operators with multiple machines should review effective rates per machine or per location. High-interchange locations (airports, stadiums) may warrant separate payment accounts or price adjustments, while low-interchange locations can leverage small ticket programs effectively.

Questions to ask your data:

- Which machines have the highest effective processing rates?

- Which locations generate the most premium rewards card transactions?

- Which machines consistently qualify for small ticket interchange?

- Should high-interchange locations be on a separate payment account?

Operators using vending management software with real-time sales tracking and transaction reporting can answer these questions quickly and adjust strategy as needed.

What Most Vending Operators Get Wrong About Processing Fees

Focusing Only on the Percentage Rate While Ignoring the Flat Per-Transaction Fee

A processor advertising "1.5%" can still be more expensive than one charging "2.6% + $0.10" for small-ticket vending sales, depending on your average transaction size.

You must calculate the effective rate using your actual average ticket size and transaction volume, not just compare headline percentages.

Example:

On a $1.75 transaction:

- Processor A (1.5% + $0.15): $0.03 + $0.15 = $0.18 total (10.3% effective rate)

- Processor B (2.6% + $0.10): $0.05 + $0.10 = $0.15 total (8.6% effective rate)

Despite the lower percentage, Processor A is more expensive because the flat fee is higher.

Assuming All Locations and Cards Should Be on the Same Processor Plan

Card mix and average ticket size vary by location — a one-size-fits-all account treats every machine the same, even when they perform very differently. Segmenting accounts by transaction profile lets lower-volume machines qualify for small ticket interchange programs.

Consider this scenario:

- 17 standard machines averaging $2.00 tickets → qualify for small ticket rates

- 3 airport machines averaging $10+ tickets with premium rewards cards → routed to a separate account

Keeping those 3 high-cost machines in the same account pulls up your fleet-wide effective rate. Separating them protects the 17 from absorbing that cost.

Underestimating the Hidden and Recurring Costs Beyond the Per-Transaction Rate

Cellular data fees, PCI compliance fees, hardware leasing, and monthly minimums can significantly change the true cost of accepting cards. Factor all of these into every processor comparison — not just the transaction rate.

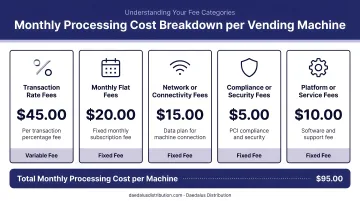

Example total cost per machine per month:

- Transaction fees: $75 (based on 100 transactions at $2.00 avg, 5.95% rate)

- Monthly service fee: $9.95

- Cellular data: $7.95

- PCI compliance: $5.00 (if charged separately)

- Total: $97.90/month

That $97.90 monthly figure tells you far more than a headline rate ever will — use it as your apples-to-apples benchmark when evaluating any processor.

Frequently Asked Questions

Do vending machines have credit card fees?

Yes, vending machine operators pay credit card processing fees on every cashless transaction—typically a combination of a percentage of the sale plus a flat per-transaction fee. These fees are paid by the operator (the merchant), not the customer, unless the operator has implemented a surcharge or tiered cashless pricing.

Who pays the 3% credit card fee?

The vending machine operator pays processing fees to their payment processor, which splits the fee among the issuing bank (interchange), card network (assessment), and processor (markup). Some operators pass part of this cost to customers through surcharges, though doing so is subject to state laws and disclosure requirements.

Is a 3% transaction fee a lot?

In retail contexts, 3% sounds modest. But in vending—where the average transaction is under $2.25—the effective fee rate (including flat per-transaction components) can exceed 8-10% of revenue. For operators running on 20-30% net margins, that easily wipes out one-third of gross profit on a single sale.

What is the 2% charge on credit card payment?

A "2% charge" typically refers to the interchange portion of the processing fee—the amount paid to the card-issuing bank. It's just one component; card network assessments (around 0.10%) and the processor's markup push the total effective rate higher.

Is it illegal to charge a 3% credit card fee?

Surcharges are legal in most U.S. states but prohibited in Connecticut, Massachusetts, and Puerto Rico. Where permitted, they must be disclosed before the transaction, capped at the lesser of your merchant discount rate or 3%, and meet card network rules—including minimum font size requirements on unattended terminals.